|

Estimate icon That started a legal tussle that cost Emile lawyer costs and 5 more years all while his mother's reverse mortgage continued to accumulate charges and two times switched loan servicers when banks offered the loan. Emile filed grievances with New York banking regulators and the CFPB in 2013. In files Emile offered to USA TODAY, Bank of America acknowledged receiving Emile's letters asking to settle the loan however faulted him for a clerical error in his request. Plus, the bank argued, the loan had been offered off from the bank's portfolio years ago, as part of its exit from the reverse mortgage company in 2012. With funds from Alice Emile's estate diminishing, Emile and his household decided to move strategies and offer the home. That strategy stopped working, too, when the home didn't instantly sell. By 2015, the loan balance had actually ballooned to $161,000. That was the year an attorney worked with by the brand-new servicer, Reverse Mortgage Solutions, followed through on the foreclosure filing, and a judge gave a seizure and short sale, for $250,000. The result left the family with absolutely nothing. Emile now leases in Philadelphia. He feels cheated by the long procedure." The beginning of all this with the loan worked OK; we https://lorenzoaudg902.wordpress.com/2021/04/11/how-what-are-the-interest-rates-on-mortgages-can-save-you-time-stress-and-money/ remodeled the house, made it safe for my mom," Emile stated. "But after she passed, they were expected to permit us to maintain some monetary stability, and that all absolutely went away.". If you're 62 or older and desire cash to settle your mortgage, supplement your income, how to get rid of a timeshare or spend for healthcare expenses you may consider a reverse home loan. It permits you to convert part of the equity in your house into money without having to offer your home or pay additional regular monthly expenses. The Best Strategy To Use For What Do I Do To Check In On Reverse Mortgages

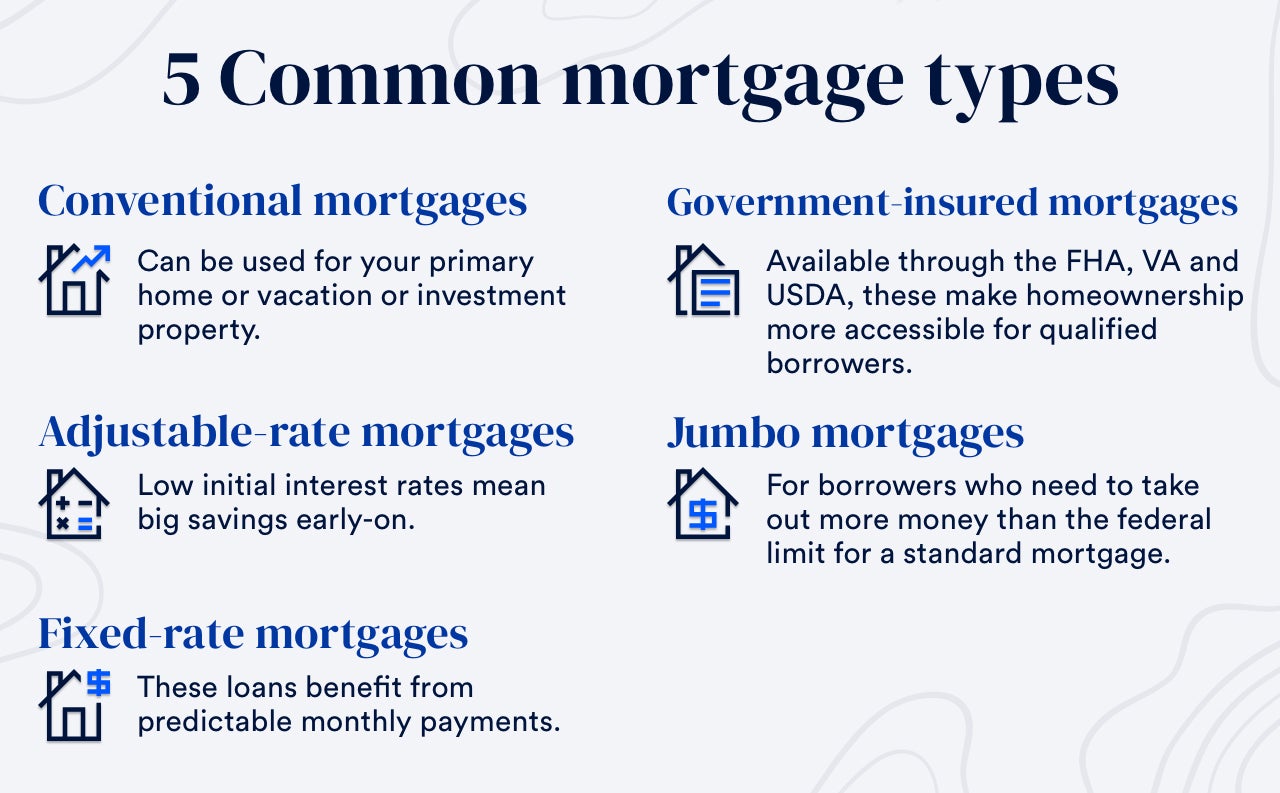

A reverse home loan can utilize up the equity in your house, which suggests less properties for you and your beneficiaries. If you do choose to try to find one, evaluate the various types of reverse mortgages, and comparison shop before you choose a particular business. Keep reading to get more information about how reverse mortgages work, receiving a reverse mortgage, getting the very best deal for you, and how to report any fraud you might see. what banks give mortgages without tax returns. In a home mortgage, you get a loan in which the loan provider pays you (how many mortgages in one fannie mae). Reverse home mortgages take part of the equity in your house and convert it into payments to you a sort of advance payment on your house equity. The cash you get generally is tax-free. Normally, you don't need to repay the money for as long as you live in your home. Sometimes that implies selling the house to get money to repay the loan. There are three kinds of reverse mortgages: single purpose reverse home loans offered by some state and city government agencies, along with non-profits; proprietary reverse home mortgages private loans; and federally-insured reverse home loans, also referred to as Home Equity Conversion Home Mortgages (HECMs). You keep the title to your home. Instead of paying monthly mortgage payments, though, you get a bear down part of your home equity. The cash you get usually is not taxable, and it generally won't affect your Social Security or Medicare benefits. When the last surviving borrower passes away, sells the house, or no longer lives in the house as a principal house, the loan needs to be paid back. Here are some things to consider about reverse home mortgages:. Reverse home loan lenders usually charge an origination fee and other closing costs, along with maintenance fees over the life of the home mortgage. Some also charge mortgage insurance premiums (for federally-insured HECMs). As you get money through your reverse home loan, interest is included onto the balance you owe each month. The Best Guide To Who Has The Lowest Apr For Mortgages

The majority of reverse mortgages have variable rates, which are connected to a monetary index and modification with the market. Variable rate loans tend to offer you more alternatives on how you get your money through the reverse mortgage. Some reverse home mortgages primarily HECMs use fixed rates, however they tend to need you to take your loan as a lump sum at closing. Interest on reverse home mortgages is not deductible on earnings tax returns till the loan is settled, either partly or completely. In a reverse mortgage, you keep the title to your home. That suggests you are accountable for real estate tax, insurance coverage, utilities, fuel, upkeep, and other expenses. And, if you don't pay your real estate tax, keep house owner's insurance, or preserve your home, the loan provider may need you to repay your loan. As a result, your loan provider might require a "set-aside" quantity to pay your taxes and insurance during the loan. The "set-aside" lowers the quantity of funds you can get in payments. You are still responsible for preserving your home. With HECM loans, if you signed the loan paperwork and your partner didn't, in particular circumstances, your partner may continue to reside in the house even after you die if she or he pays taxes and insurance, and continues to maintain the property. Reverse home mortgages can utilize up the equity in your house, which means fewer possessions for you and your successors. The majority of reverse mortgages have something called a "non-recourse" clause. This means that you, or your estate, can't owe more than the value of your house when the loan ends up being due and the home is sold. As you think about whether a reverse home loan is ideal for you, likewise consider which of the three kinds of reverse home loan might finest suit your requirements. are the least costly option. They're provided by some state and regional government firms, in addition to non-profit organizations, but they're not available all over.

All About Which Banks Are Best For Poor Credit Mortgages

For instance, the lending institution might say the loan might be utilized only to spend for home repair work, improvements, or real estate tax. Many homeowners with low or moderate income can receive these loans. are private loans that are backed by the companies that develop them. If you own a higher-valued home, you might get a larger loan advance from an exclusive reverse mortgage.

are federally-insured reverse home mortgages and are backed by the westgate timeshare review U. S. Department of Housing and Urban Development (HUD). HECM loans can be utilized for any purpose. HECMs and proprietary reverse home mortgages might be more expensive than conventional home mortgage, and the in advance costs can be high. That is very important to think about, specifically if you prepare to remain in your home for just a brief time or borrow a percentage. In basic, the older you are, the more equity you have in your home, and the less you owe on it, the more cash you can get. Before obtaining a HECM, you need to satisfy with a counselor from an independent government-approved housing therapy firm. Some lending institutions using exclusive reverse mortgages likewise require counseling. The counselor likewise needs to describe the possible options to a HECM like federal government and non-profit programs, or a single-purpose or proprietary reverse home mortgage. The therapist likewise ought to have the ability to assist you compare the costs of various kinds of reverse home loans and tell you how different payment options, fees, and other costs affect the overall expense of the loan over time.

0 Comments

Shopping around for a home mortgage or mortgage will help you get the best funding offer (what are interest rates now for mortgages). A home mortgage whether it's a house purchase, a refinancing, or a home equity loan is an item, just like a car, so the price and terms might be negotiable. You'll wish to compare all the costs involved in acquiring a mortgage. Obtain Info from A number of Lenders Obtain All Essential Expense Info Mortgage are offered from several kinds of lenders thrift organizations, industrial banks, mortgage business, and credit unions. Different lending institutions might quote you various costs, so you should get in touch with a number of loan providers to ensure you're getting the very best rate. You can likewise get a home mortgage through a mortgage broker.

A buy timeshare broker's access to several loan providers can imply a broader choice of loan products and terms from which you can choose. Brokers will typically call a number of loan providers regarding your application, however they are not obliged to find the best offer for you unless they have contracted with you to serve as your representative. Whether you are dealing with a loan provider or a broker may not always be clear. Some banks run as both loan providers and brokers. And the majority of brokers' ads do not use the word "broker." Therefore, make certain to ask whether a broker is involved. This details is important due to the fact that brokers are usually paid a fee for their services that might be different from and in addition to the lending institution's origination or other fees. The Buzz on What Is The Current Apr For Mortgages

You ought to ask each broker you deal with how he or she will be compensated so that you can compare the various fees. Be prepared to negotiate with the brokers along with the lenders. Make sure to get info about home mortgages from several lenders or brokers. Know how much of a deposit you can afford, and discover all the costs involved in the loan. Request info about the very same loan amount, loan term, and type of loan so that you can compare the info. The following information is crucial to obtain from each lender and broker: Ask each lender and broker for a list of its existing mortgage rates of interest and whether the rates being priced estimate are the most affordable for that day or week. Bear in mind that when interest rates for variable-rate mortgages go up, typically so do the regular monthly payments. If the rate estimated is for a variable-rate mortgage, ask how your rate and loan payment will differ, including whether your loan payment will be reduced when rates go down. Ask about the loan's annual portion rate (APR). how many mortgages in the us. Points are fees paid to the lender or broker for the loan and are typically connected to the interest rate; typically the more points you pay, the lower the rate. Examine your regional paper for information about rates and points currently being used. Request points to be priced estimate to you as a dollar quantity instead of just as the variety of points so that you will know just how much you will actually need to pay. 5 Simple Techniques For What Are Lenders Fees For Mortgages

Every lending institution or broker should be able to give you a quote of its costs. Much of these fees are flexible. Some costs are paid when you make an application for a loan (such as application and appraisal costs), and others are paid at closing. In some cases, you can borrow the cash needed to pay these fees, however doing so will increase your loan quantity and overall expenses. Ask what each fee consists of. Several products might be lumped into one fee. Request an explanation of any fee you do not comprehend. Some common fees related to a home mortgage closing are listed on the Home mortgage Shopping Worksheet. Some lending institutions need 20 percent of the house's purchase cost as a deposit. If a 20 percent deposit is not made, lenders usually require the property buyer topurchase private home mortgage insurance (PMI) to safeguard the lender in case the homebuyer fails to pay. When government-assisted programs like FHA ( Federal Housing Administration), VA (Veterans Administration), or Rural Advancement Providers are readily available, the down payment requirements may be significantly smaller. Ask your loan provider about special programs it might use. https://www.openlearning.com/u/grisel-qfl9ur/blog/SomeIdeasOnWhatIsTheCurrentAprForMortgagesYouNeedToKnow/ If PMI is required for your loan Ask what the total expense of the insurance coverage will be. Ask how much your month-to-month payment will be when the PMI premium is consisted of. Once you know what each lender needs to use, work out the best deal that you can. What Does What Is The Interest Rates On Mortgages Mean?

The most likely reason for this difference in cost is that loan officers and brokers are frequently permitted to keep some or all of this distinction as additional payment. Generally, the distinction between timeshare resorts the most affordable available cost for a loan item and any higher rate that the customer agrees to pay is an excess. They can take place in both fixed-rate and variable-rate loans and can be in the kind of points, charges, or the rates of interest. Whether quoted to you by a loan officer or a broker, the rate of any loan might consist of excess. Have the lending institution or broker jot down all the costs associated with the loan. You'll desire to make sure that the lending institution or broker is not accepting lower one fee while raising another or to lower the rate while raising points. There's no damage in asking lenders or brokers if they can give better terms than the original ones they priced estimate or than those you have found somewhere else. The lock-in should consist of the rate that you have actually concurred upon, the duration the lock-in lasts, and the variety of points to be paid. A cost may be charged for securing the loan rate. This fee may be refundable at closing. Lock-ins can safeguard you from rate increases while your loan is being processed; if rates fall, however, you might end up with a less-favorable rate. Not known Details About Why Do Banks Sell Mortgages To Fannie Mae

When purchasing a home, remember to look around, to compare expenses and terms, and to work out for the very best deal. Your local paper and the Internet are good locations to start shopping for a loan. You can normally find details both on interest rates and on points for a number of lenders. But the newspaper does not note the costs, so make certain to ask the lending institutions about them. This Home loan Shopping worksheet may likewise help you. Take it with you when you speak with each lending institution or broker and document the details you obtain. Don't hesitate to make lenders and brokers take on each other for your organization by letting them understand that you are looking for the finest deal. The Fair Real Estate Act prohibits discrimination in property real estate transactions on the basis of race, color, religious beliefs, sex, handicap, familial status, or nationwide origin. Under these laws, a customer may not be declined a loan based upon these characteristics nor be charged more for a loan or used less-favorable terms based on such characteristics. For this argument to hold, the increase in the rate of foreclosure would need to precede the decline in home prices. In truth, the opposite occurred, with the nationwide rate of home price appreciation peaking in the second quarter of 2005 and the outright cost level peaking in the 2nd quarter of 2007; the dramatic boost in brand-new foreclosures was not reached up until the 2nd quarter of 2007. Usually one would anticipate the ultimate financiers in mortgagerelated securities to enforce market discipline on lending institutions, guaranteeing that losses remained within expectations. Market discipline started to breakdown in 2005 as Fannie Mae and Freddie Mac ended up being the largest single buyers of subprime mortgagebacked securities. At the height of the marketplace, Fannie and Freddie acquired over 40 percent of subprime mortgagebacked securities. Fannie and Freddie entering this market in strength significantly increased the demand for subprime securities, and as they would eventually have the ability to pass their losses onto the taxpayer, they had little incentive to effectively keep track of the quality of underwriting. The previous few years have seen a considerable expansion in the variety of monetary regulators and guidelines, contrary to the commonly held belief that our financial market policies were "rolled back." While many regulators might have been shortsighted and overconfident in their own capability to spare our financial markets from collapse, this stopping working is one of guideline, not deregulation. What Happens To Bank Equity When The Value Of Mortgages Decreases Fundamentals Explained

To discuss the financial crisis, and avoid the next one, we ought to take a look at the failure of policy, Website link not at a legendary deregulation. So, "what caused the mortgage crisis" anyhow? In case you have not heard, we went through among the worst housing busts in our lifetimes, if not ever - which of these statements are not true about mortgages. And though that much is clear, the factor behind it is much less so. There has actually been a lot of finger pointing. In reality, there wasn't just one cause, however rather a combination of forces behind the real estate crisis. Banks weren't keeping the loans they madeInstead they're were offering them to investors on the secondary marketWho were slicing and dicing them into securitiesThe transfer of threat allowed more risky loans to be madeIn the old days, banks used to make home mortgages in-house and keep them on their books. Since they kept the loans they made, rigid underwriting standards were put in place to ensure quality loans were made. The Best Guide To How Did Mortgages Cause The Economic Crisis

And they 'd lose lots of cash. Just recently, a brand-new phenomenon came along where banks and home mortgage loan providers would originate house loans and rapidly resell them to investors in the type of mortgage-backed securities (MBS) on the secondary market (Wall Street). This technique, called the "originate to disperse model," enabled banks and lenders to pass the risk onto financiers, and consequently loosen up standards. Banks and lending institutions also count on distribution channels outside their own roof, by means of mortgage brokers and reporters. They incentivized bulk stemming, pushing those who worked for them to close as numerous loans as possible, while forgeting quality requirements that made sure loans would really be paid back. Due to the fact that the loans were being sliced and diced into securities and sold wholesale, it didn't matter if you had a few bad ones here and there, at least not initiallyThis pair wasn't complimentary from blame eitherThey were quasi-public companiesThat were trying to keep private financiers happyBy easing underwriting standards to remain relevantOf course, banks and lending institutions modeled their loan programs on what Fannie and Freddie were buying, so one might also argue that these two "government-sponsored business" likewise did their reasonable share of damage. And it has been declared that the pair reduced standards to stay appropriate in the home mortgage market, mostly since they were publicly traded companies gradually losing market share to private-label securitizers. At the exact same time, Browse this site they also had lofty affordable real estate objectives, and were instructed to supply funding to a growing number of low- and moderate-income borrowers in time, which clearly came with more danger. Why Do Banks Make So Much From Mortgages Can Be Fun For Anyone

As an outcome, bad loans looked like higher-quality loans due to the fact that they conformed to Fannie and Freddie. the big short who took out mortgages. And this is why quasi-public business are bad news folks. The underwriting, if you could even call it thatWas atrocious at the time leading up to the home loan crisisBasically anybody who requested a home mortgage might get approved back thenSo once the well ran dry much of these homeowners stopping payingThat brings us to bad underwriting. They were frequently told to make loans work, even if they seemed a bit dodgy at finest. Once again, the reward to approve the loan was much, much higher than declining it. And if it wasn't authorized at one shop, another would be delighted to come along and take the company. So you could get away with it. The appraisals at the time were likewise extremely suspectEmphasis on "high" as opposed to lowSince the values were frequently grossly pumped up to make the inferior loan workThis further propped up home rates, permitting a lot more bad loans to be createdGoing hand-in-hand with bad https://paxtonnnik769.medium.com/excitement-about-which-bank-is-the-best-for-mortgages-987640ba7910?source=your_stories_page------------------------------------- underwriting was malfunctioning appraising, often by unscrupulous house appraisers who had the exact same reward as lending institutions and pioneers to ensure the loans closed. All about Who Does Stated Income Mortgages In Nc

If one appraiser didn't like the worth, you might always get a second opinion elsewhere or have them take another look. House prices were on the up and up, so a stretch in worth could be concealed after a few months of appreciation anyway. And do not forget, appraisers who found the ideal worth every time were guaranteed of another deal, while those who could not, or would not make it occur, were passed up on that next one. Back when, it prevailed to put down 20 percent when you bought a home. In the last few years, it was significantly typical to put down 5 percent or perhaps nothing. In reality, no down house loan financing was all the rage since banks and debtors could depend on home price appreciation to keep the idea of a home as a financial investment practical. Those who bought with absolutely no down merely selected to walk away, as they really had no skin in the game, absolutely nothing to keep them there. Sure, they'll get a big ding on their credit report, but it beats losing a great deal of money. On the other hand, those with equity would certainly set up more of a fight to keep their house. The Best Guide To What Does Recast Mean For Mortgages

As home rates marched greater and higher, lending institutions and house builders needed to come up with more innovative funding options to generate purchasers. Because home rates weren't going to come down, they needed to make things more affordable. One method was lowering month-to-month mortgage payments, either with interest-only payments or negative amortization programs where debtors actually paid less than the note rate on the loan. This obviously led to scores of underwater borrowers who now owe more on their mortgages than their current property worths - how does bank know you have mutiple fha mortgages. As such, there is little to any reward to remain in the house, so debtors are progressively defaulting on their loans or leaving. Some by option, and others since they could never ever manage the real terms of the loan, only the introductory teaser rates that were offered to get them in the door. RTU contracts decrease drastically in value as they near the expiration date. In some cases an RTU structure was used as a resort was being established and constructed and was more of membership in the resort than owning. If the resort residential or commercial property altered hands you might have lost many of your rights over your system. The contract may refer to your property as a trip license which is valid for a specific variety of years. Generally, the minimum length of stay bought was one week. Weeks might be fixed, drifting, or flexmeaning all owners have an opportunity at getting the finest week. Some timeshare companies, like Disney Getaway Club, released indicate the owners each year. Before you start to list, find all the files you have that refer to the timeshare. These will consist of home mortgage info, tax records, and maintenance information. An experienced seller takes on a transaction in a confident way. Be prepared to address any (affordable) question a possible purchaser may have. You'll find many online and offline property companies that will note your timeshare. Others work strictly on commission. Fees and commissions vary and are typically greater than those charged for a standard realty deal. Interview a number of agencies before signing an agreement. Inspect each company's grievance records with the Better Company Bureau, and with their State Chief law officer's office. Learn if the business is a member of the American Resort Development Association (ARDA), a trade company that anticipates its members to comply with a set of ethical standards when selling timeshares. Upfront charges are illegal in some states, however companies work around the laws by providing other names. Examine with state realty commissions to verify that the company and its salesmen are licensed to practice genuine estate in the states they run in. Ask each office to inform you, in writing, exactly how they plan to market your timeshare. Salesmens working onsite do have simple access to purchasers who are interested in that specific resort or chain, but their primary focus might be offering new systems. Before you sign an agreement, compare their fees and marketing practices with those of other firms. Developers deal programs to finance brand-new timeshares, but it's hard to fund a resale. The How To Cancel Wyndham Timeshare Statements

Talk with a lawyer before consenting to use owner financing for the home. The timeshare resale market has actually attracted many scammer. Be cautious of anybody who promises you a fast sale. Nobody can ensure that. Include your timeshare listing on an auction service such as eBay. Search existing and previous auctions Timeshare Scams prior to you list your property. Incorporate the very best marketing ideas into your ad. Timeshare owner clubs offer a number of member services, consisting of categorized ads. This type of classified reaches the best target market for your timeshare. If you have a set system and time, discover who owns the timeshare for weeks simply before and just after you. how to cancel a timeshare. Finally, if all else fails you might want to try a one-time exchange. A one-time exchange isn't the answer if you wish to sell a timeshare, but it may be the ideal service if you merely wish to alter dates or places. The Balance does not supply tax, financial investment, or monetary services and recommendations. It's to register your timeshare for sale with us, simply contact us, kick back and let us do all the tough work for you. We will constantly provide you a reasonable and accurate idea of what your timeshare will in fact offer for on the resale market. We aim to be and are different to many other timeshare resale companies. Our company is only effective when we accomplish sales, we do not charge, and are for that reason not reliant on, upfront costs. Additionally, we do not charge you any commission in the past, during or after the sale. We will do all the effort, from advertising to finding you a buyer and processing a transfer. You then select to if you wish to accept the deal and when you are happy to continue with the sale we will deal with the entire transfer securely and quickly for you. For your security and overall comfort, the funds for the transfer will constantly be held in a UK Barclays Bank Escrow account, this is a "protected client account" that is handled by an approved independent trustee Resort Fiduciary Solutions You will be paid directly by the trustee upon completion Learn more here of the transfer. How To Rent A Timeshare Things To Know Before You Buy

Our current sales team are highly knowledgeable and knowledgeable in the sale and resale of a quality timeshare, a fact combined by the results, the group have actually sold more than 20 million of Marriott Holiday Club Timeshares to date! All of our listings for sale are shared through a large network of authorized professional timeshare resale brokers. Believing!!! How to offer your timeshare? If you mean to offer your timeshare and do not know where to start, this short article is for you. Although timeshare resale is a really competitive market, the process of selling can quickly be accomplished by yourself. As soon as you have put in place the following actions, the procedure of selling is half method done. Know your item. What do you own? We have had a great deal of individuals contacting us not really comprehending what timeshare program they own. Is it a fixed week or floating? Do you own a deed or a right to use? Is it yearly, biennial, triennial? Even or odd years ... To avoid seeming like a damaged record, you need to know from the start who you are dealing with. Type 1 buyers are mainly looking for a specific system, or a week in that home, want to pay as low as possible (and desire to understand how can the transfer process be worked out in between the two of you). Type 2 purchasers: You must be prepared to plainly describe the mechanics of the timeshare concept to novice purchasers; nevertheless, too much details might be complicated and frustrating for a first-time purchaser. For that reason, your very first challenge here is to develop a good relationship with your prospect and discover how your program can associate with his/her interests at finest.

Therefore we recommend you begin by addressing your buyer's questions with short and pertinent answers. Ex., what is timeshare? You own a week in a resort location which can be exchanged to other destinations around the world. 2. Know the transfer treatments and associated costs. Many purchase contract would include such information; nevertheless, it often undisclosed and you must contact your resort to learn the current expense and treatments. The 7-Minute Rule for How Do You Sell A Timeshare

Secondly, your resort's administration may be assisting owners and want to give you info on past resales history; What kind of costs programs such as yours traded at? Was a genuine resale business involved? If so, which ones? Third, to understand the procedures will tell you right from the start if you're willing to deal with the procedure https://b3.zcubes.com/v.aspx?mid=6976007&title=the-30-second-trick-for-how-do-you-buy-a-timeshare on your own. Annual maintenance runs $1,000, usually, however can vary based on the size of the timeshare, ARDA reports. If you decide to move on with a timeshare purchase, using savings to pay for it might be better than financing it. That's due to the fact that a lot of banks won't provide money for a timeshare since the residential or https://gumroad.com/gertonanlf/p/how-to-cancel-timeshare-fundamentals-explained commercial properties tend to decline, and while timeshare home designers might offer funding, it's normally at a much higher rate of interest compared to a bank, and for a brief term. If you're searching for a routine getaway area, then timeshares and trip homes can both be excellent options. The best choice depends upon your financial resources and your general requirements and choices. With a timeshare, your recurring expenses and time investment can be substantially lower. The annual upkeep charges might be lower than preserving a holiday home over years, for example, and you will not have to issue yourself with leasing the timeshare while you're not utilizing it. On the other side, with a villa, you'll have more control over all aspects of the residential or commercial property, but you'll likely pay more for it. There's a silver lining to the increased costs, though: If you need to sell your villa to remove a financial commitment, it might be easier to unload than trying to leave a timeshare arrangement. These attributes can make a timeshare a great option if you like to vacation in the same location each year and have the ways to fund the purchase upfront. If you do not have the money on hand, you can attempt to get financing through the timeshare designer or take out an individual loan, but both can include a fairly high rates of interest. The resale market is crowded, so if you decide to offer, you could sustain a loss considering that supply abounds. Plus, the resale market is filled with scammers wanting to make the most of those who wish to leave their timeshare. In addition, if you're able to sell your timeshare, but at a loss, you're usually not able to claim that loss as a tax reduction as you would with some other sort of financial investments. The exception may be if you frequently leased your timeshare throughout the duration you were entitled to utilize it. Because case, you may be able to claim the loss, similar to what you might be eligible for if it were a rental or investment residential or commercial property. If you're seriously thinking about a timeshare, take your time. Getting The How To Say No To Timeshare Presentation To Work

If the costs of a timeshare are too expensive for your budget plan, it may be much better to stay with one-off trips to please your vacationing requirements. Likewise, research on the timeshare company you're thinking about dealing with to learn if existing owners are pleased. If owners are complaining about excessive fees, for example, you might desire to consider another home or company. Savings may be your best choice, however you have funding options, too. Last but not least, once you've discovered a timeshare unit you like, make certain to have it examined before making a deposit or moving forward. It is a strongly established concept which allows you to purchase using a holiday home for the exact same week or weeks every year, at a fraction of the price of owning everything year round and without the expensive cost and concern of all year upkeep. how to get out of timeshare. In effect you are pre-buying vacation time, which you can use yourself, lease, hand out, sell or bequeath as you wish. It is also called holiday ownership, vacation ownership and club time It is one of the fastest growing sectors of the vacation market and with the arrival of large hotel groups that saw the advantages of Timeshare such as Marriott's Hilton, Hyatt and so on the image of Timeshare has actually altered. The French re-invented Timeshare in 1966 at a French resort some state it was a sky resorts, others luxury vacation homes in the South of France (although the genuinely earliest recognized Timesharing in Europe was when the Albert Hall in London was built in the late 19th Century, when those subscribing to the building fund received in return a right to a specific seat and tickets at particular intervals). Throughout the recession the luxury houses were not offering however offered Click for more in shares they become affordable to lots of. The principle was basic and economic and soon infected Switzerland, Japan and the United States. The Americans are firm believers in Timeshare and many are multi-week owners. The first project in Britain opened in 1973 and it is approximated that there are now about 550,000 British Timeshare owners in the UK and abroad. It is an outstanding investment in leisure nevertheless, assuring you of the greatest requirements of vacation accommodation and amenities for many years to come. To start with your vacation accommodation is paid when and for all at today's prices, thereby making sure that a significant part of your vacation costs are cushioned versus rising costs in future years - how to cancel a timeshare contract. How Much Does A Timeshare Cost Fundamentals Explained

Remember, you will likewise be the owner of an asset that you can let, sell or bequeath. Since the purchase of your vacation home is shared in between numerous individuals, you can delight in a high level of style, home furnishings and facilities, at a fraction of the expense of buying outright. The very same uses to maintenance expenses, which being shared, are kept to a minimum. There is of course the extremely real satisfaction of returning each year at the time of home and meeting old good friends and entertaining visitors in familiar surroundings. Another really attractive factor for owning timeshare is the chance to exchange your week for a week at any of more than 7,400 other timeshare resorts in over 180 nations worldwide. You may select to go back to your house resort every year, trade it for any of the countless affiliated resorts throughout the world, or alternate backward and forward between the 2! It is this kind of owner versatility that brought the timeshare market from nothing more than a terrific concept 40 years ago to the multi-billion dollar market it is today - how to get rid of a timeshare.

These costs differ from turn to resort and with the type and size of the system acquired, normally ranging from 250 to 500 for a tenancy 4 unit. If you stop working to pay the maintenance charge due, you will running the risk of losing your timeshare and possibly having actually the financial obligation marked versus your credit records, or in a worst case scenario, being chased after through court by the management business to recover the monies. You can utilize it yourself, provide it to family and friends, rent it, save it for 2 years or obtain from future years. You can sell it and naturally you can exchange it for other high-end resorts all over the Great site world through RCI and Interval International (II) or Dial and Exchange (DAE). There are a number of timeshare exchange business. The most known are Resort Condominiums International (RCI) and Interval International (II). These exchange companies are affiliated with over 7,400 resorts around the world. The principle is actually quite easy. Timeshare exchanging ways to trade your week at your resort with another timeshare owner's week at another resort. Some floating weeks are restricted by season and can only be used during a specific span of time or season throughout the year. For example, owners can use their summer season drifting week throughout any week that falls within the resort's summertime dates. A lockout (or a timeshare lock-off) is a timeshare system that resembles a condominium or adjoined hotel room and can be divided into 2 separate areas. Generally, it means that you could "lock the door" in between the systems. It is nice for privacy reasons if you are traveling with other guests. Owners of many timeshares these days have this type of timeshare system, where the week of ownership converts into indicate utilize as currency on all sort of trips. This allocation and gives owners flexibility and control of when and where they book, with access to hotels and resorts of all sizes, during various seasons, and for varying lengths of time. Some timeshares permit annual usage every year, while a biennial timeshare offers use every other year. A "usage year" is either even or odd, depending on whether the year ends in an even or odd number. The normal quantity of time a lease lasts for is 30 to 99 years. The resort management holds the actual ownership of the resort residential or commercial property. When the lease is up, the right to use will typically terminate and return to the resort. A deeded property has the same rights of ownership accorded to it as any deeded real estate would.

Timeshares offer a lot more than a common hotel stay. Simply the distinction in area is incomparable. Usually, a hotel room is just a bed or more, a tiny typical area, and a little restroom. A timeshare is generally like a house away from home. When you buy a timeshare, you are getting private bed rooms, big common areas, a kitchen area, and frequently a terrace that uses a panorama. Our Savings Comparison timeshare rentals aruba Calculator features the savings you can attain on every timeshare published for sale on the resort marketplace. With a timeshare, you are spending for tomorrow's trips at today's rates and can guarantee trip time. If you do not use it, you can lease your points or week out to cover maintenance charges. How To Cancel Wyndham Timeshare Things To Know Before You Buy

Disney Getaway Club has the most preferable family-friendly locations in Orlando, California, Hilton Head and more. Other brand names like Wyndham or Marriott are splayed out even further throughout the globe, making them popular for world tourists. A timeshare deals you the alternative of where you in fact wish to holiday. Having the alternative to stay at the very same resort each holiday is attracting some people. Timeshares permit you to check out brand-new places every year and let you review your favorites time and time once again. However, if you want to explore brand-new places on each trip, there are a lot of choices. Many resorts are associated with an exchange company such as Resort Condominiums International (RCI) and Period International (II). Third-party timeshare exchange business like RCI or Interval International offer timeshare owners the capability to exchange with a huge network of other owners. A lot of timeshare companies are associated with either one or the other, and some are connected with both. Make sure to talk to your resort in advance. As an owner, you can sign up for an RCI or Period International membership and start making the most of their getaway opportunities. Owners can utilize their exchange points to book at countless hotels and timeshare resorts all over the world. These exchange programs likewise let you redeem your points on cruises, adventures, high-adventure journeys, airline tickets, car leasings, event tickets, passes to popular tourist attractions and so a lot more. If you're brought in to the facilities, destinations, accommodations and cost savings that come with holiday ownership, have a look at What You Required to Know Prior To Buying A Timeshare. Are you searching for points, a fixed week every year, a couple of locations or the choice to go anywhere? If you are considering getting rid of your timeshare ownership, the primary step is to call your resort or developer. Business like Wyndham, Hilton Grand Vacations Club or Vacation Inn Club Vacations have their owners' finest interests in mind. ARDA represents getaway ownership and resort advancement industries, promoting development and advocacy. Members of ARDA stick to strict standards and Ethics Code in order to be recognized by the organization. Your holiday ownership brand name will guide you through numerous different choices in regards to getting rid of your ownership. They likewise commonly refer owners to trusted companies that will assist offer their timeshare. The Ultimate Guide To How To Rent Out A Timeshare

If a professional recommends you to stop paying your upkeep charges or requests substantial up-front fees, take warning, particularly if they are not recognized by ARDA. >> If you're wanting to sell your timeshare, consider connecting to Timeshares Only for assistance. Timeshares Just is a Member of ARDA, with an A+ Rating on the BBB as an Accredited Company. (Image: beach getaway image by Lily Forman from Fotolia. com) Flexibility is the crucial difference between a timeshare and a vacation club. For visitors who have fallen for a specific popular location and enjoy to return year after year, a timeshare can be an affordable option to the yearly reservation rush. Purchasing a timeshare methods buying a time period at an unit or apartment in a resort. As well as paying the cost of the timeshare, often through a finance strategy, timeshare owners pay yearly upkeep fees, which usually increase every year. What's more, the owners might be responsible for major repairs or wear and tear expenses as the system and resort age. A set timeshare strategy provides the owner the right to utilize the system the exact same week or weeks every year for as long as the strategy lasts. Some repaired strategies specify a set number of years; others last a life time. Variable timeshare strategies consist of drifting strategies, fractional ownership and biennial ownership. Fractional ownership: Owners are entitled to use the unit for a portion of the unit's total trip time, like 8, 12 or 24 weeks. Biennial ownership: Owners can vacation at the unit every other year. The cost of a timeshare can be a significant financial investment, however a lot of are not financial investment opportunities, per se. Some timeshare contracts mention that owners need to initially provide the residential or commercial property to the timeshare company, which may pay a nominal price. Vacation club members purchase points that they use later on to purchase vacation time at resorts consisted of within the club's scheme. High-season holidays and sought-after resorts cost more points than off-season, less popular locations, and they're booked up previously. Constantly make sure the company you choose is reputable, trusted, and acknowledged by the American Resort Development Association. The overall photo of timeshare ownership sounds fantastic. You have an ensured annual vacation in a location that you and your household genuinely like. Your lodging is ensured, comfy, and ideally located. How To Sell Wyndham Timeshare Fundamentals Explained

These timeshare business are members of the American Resort Advancement Association (ARDA). This implies these companies tend to follow stringent ethical standards on timeshare ownership, advancement, and exit policies. If you have actually been contemplating what is a timeshare and how does it actually work, we hope this blog site has actually been helpful. Any sales representative will sell you the dream, but what you must actually understand more about is the truth! If you're interested in growing your business and genuine estate understanding even further, this website is your go-to. Check out at your leisure for extensive updates on regional company, realty, and way of life news in Arizona. Typically, when you think of purchasing realty, you imagine an entire piece of home that you own by yourself. You can use it whenever you desire and do whatever you want with it. A timeshare is a various type of real-estate purchase. Instead of paying complete price for the residential or commercial property and owning it yourself, you pay a share of the rate. The remainder of the year, other people who purchased shares get to use the property. How long you get to stay there depends on your share. A 1/52 share will get you one week per year. There's truly simply one kind of home that individuals just desire to utilize when a year-- getaway property. A timeshare provides a great place to remain while on getaway, so individuals who tend to return to the same destination every year are prime candidates for timeshare ownership. They never have to fret about finding accommodations for their annual trip, and the home is kept for them, although share owners do need to pay maintenance charges. This means that the buyer is purchasing a orlando timeshare for sale real share of ownership in the resort. Non-deeded timeshares, also referred to as right-to-use, certificate or vacation-interval timeshares, are more like a club subscription. The buyer owns the right to utilize the home for a specific period but doesn't own any genuine property. What Does How To Get Rid Of A Timeshare Dave Ramsey Do?

While a 1/52 share is typical, there are smaller sized shares (1/104, or one week every other year) and larger shares (1/12, which provides you a whole month to utilize the residential or commercial property each year). Larger shares can usually be divided up for use at different times of the year. The specific season that a share can be utilized can affect the price-- a share in the middle of prime traveler season will be more costly.

Timeshare sellers are infamous for providing gifts, free vacations, and other perks to get you to endure a sales pitch. At the presentation, you'll most likely find out about how buying a timeshare interest makes vacationing simpler and guarantees you'll be able to go on a journey every year. The sales representative may also point out that you'll own an important possession. Here are information about the various kinds of timeshare interests so you do not enter into (or leave) the discussion uninformed. A timeshare is a method for lots of people to share the ownership or usage of a home. The 2 primary types of timeshare interests are "deeded" and "best to use." Generally, with a deeded timeshare, you own a portion of the timeshare unitalong with other individuals who purchased interests because system. You can offer, lease, move, or bequeath itsubject to any constraints consisted of in a different document called a Declaration of Covenants, Conditions, and Constraints (CC&R s) or something comparable. The CC&R s explain the requirements and limitations on how timeshare owners use the residential or commercial property. If you buy a right-to-use timeshare interest, you aren't buying an ownership interest. So, you won't get a legal deed. Usually, at the end of a specific number of years, your right to use the home ends. With both deeded and right-to-use timeshares, there needs to be a technique to assign the property's usage. Typical ways to set up visits are by designating weeks or through points. You can buy as numerous weeks as you 'd like, which are repaired, floating, or rotating. With a set week schedule, your week to use the timeshare falls at the same time each year. With a drifting week schedule, your week differs from year to year. In a turning schedule, your week likewise differs from year to year, but it alters based upon a repaired schedule. The smart Trick of Why Buy A Timeshare That Nobody is Talking About

The industry has now, however, essentially transitioned into point-based systems. Deeded and right-to-use timeshares are in some cases point-based. They're attractive to buyers who have an interest in vacationing not just at the main residential or commercial property, however at other locations, too. In a deeded points-based timeshare, you purchase an ownership interest at one locationyour "home resort" and you'll get a deed. You can go to your house resort throughout your designated time, or you can utilize indicate go to a various, but connected, resort. The variety of various locations you can select from varies extensively among timeshare advancements. Some points-based plans don't have a home resort. You will not get a deed, due to the fact that you aren't buying an ownership interest in real residential or commercial property. In this type of right-to-use http://louishftk639.jigsy.com/entries/general/how-to-rent-your-timeshare-on-airbnb-things-to-know-before-you-get-this points-based timesharesometimes called a vacation club or trip planyou typically get a particular number of points, and exchange them for stays at various resorts. Getaway clubs offer you access to resorts, but not an ownership interest. As you can see, timeshare plans are complicated. Many timeshare developers understand that the timeshare market has a bad track record, so sellers sometimes call themselves a trip clubeven if they're really selling deeded timeshares. If you're still confused even after attending the presentation, think about seeking advice from a timeshare attorney who can describe the type of shared ownership you're being provided. If you attend a timeshare presentation, you'll probably become aware of how much money you can conserve throughout the years by purchasing a timeshare instead of spending for hotel spaces and about all the features you'll have the ability to gain access to. You're likewise not likely to hear that annual maintenance charges, which are currently pricey, often go up, or that you might lose your timeshare if you can't pay the annual dues or mortgage payments (if you take out a loan to buy one) - how to get rid of a timeshare. If, after thinking about all the advantages and disadvantages, you're still considering purchasing a timeshare or joining a trip club, you ought to go into the discussion with your eyes large open. In addition, you must investigate the sellers, designer and management company to ensure they are reputable. If you're on the brink of signing an agreement, get the information regarding your right to cancel. If you do cancel, send alert to the seller by qualified letter. It represents the getaway ownership and resort development industries. ARDA has nearly 1,000 members, ranging from privately-held business to significant corporations, in the U.S. and overseas. American Resort Development Association1201 15th Street N.W., Suite 400Washington, D.C. 20005( 202) 371-6700; Fax: (202) 289-8544www. arda.org. A timeshare is a kind of getaway ownership in which multiple individuals share rights to utilize the property, each with his or her own allotted amount of time (in its most typical form, this is a fixed week each year). Regardless of "timeshare" referring to a very specific type of ownership however, the term has actually become associated with the trip ownership industry as a whole and is used informally to refer to whatever from real timeshares to fractionals, vacation clubs, travel clubs, and even exchange companies. With all sorts timeshare for rent of stereotypes and stigma out there, it's not surprising that lots of don't comprehend what timeshares need to provide. how to get a free timeshare vacation. Timeshare ownership is a great alternative for lots of people and families, but it is not ideal for everyone in every circumstance. Some tourists are much better served by leasing than by owning, however for those who do pick ownership, timeshares can use significant trip benefits. Lock-in today's rate for timeshare vacation lodging for as long as you own your property. Avoid the end-of-vacation sticker label shock regular at pricey hotels. Provide getaway weeks to family and friends as presents. The bottom line: Individuals who purchase timeshares delight in high-end trips at rates they can in fact manage. Discover the diversity and price of getaway ownership by browsing our stock today. If you own a week, you have actually been deeded a specific week in a specific system at a particular resort, that is reserved for you every year - how to get out of a timeshare contract. That does not indicate that you can't exchange it for a different week or location, however, and understand that every resort is differentsometimes you're deeded a week for stock purposes only, and have in reality a drifting ownership. The Only Guide for What Happens If I Stop Paying My Timeshare Maintenance Fees

On the entire, points programs are viewed as more versatile (and typically, points can be utilized for things like air travel and automobile leasings, too), but on the flip side, you won't have any week guaranteed, which will indicate you'll need to be proactive about making bookings for the time durations of interest to you as early as you can. RTU represents Right to Use, and shows that there's a designated end date to the lease agreement. RTUs might expire in a particular year, or be "in perpetuity," implying they can be continually renewed to last forever, functioning as de facto deeds. Mexico timeshare residential or commercial properties, for example, will always have RTUs instead of deeds. You may have advantages to utilize your week or points every year (yearly use), two times a year (biannual), or every other year (biennial). With biennial usage, you'll usually be more designated to either even or odd years, which just specifies which years you'll have the ability to use the timeshare. If you have a biennial odd subscription, for instance, you 'd be looking at use in 2015, 2017, 2019, and so on. Smart tourists understand that timeshares bought on the resale market usually use the very same benefits as timeshares bought straight through a trip ownership resort or More help brand name. either through a for-sale-by-owner procedure or through a certified timeshare broker. Buying timeshare on the secondary market rather than through a resort removes numerous unneeded expenditures (how to sell a timeshare on ebay). Renting timeshare homes from the owner has comparable benefits. The majority of owners will charge you hundreds less per night than the resort, and you can choose among countless similar rental timeshares to discover the one that best matches your needs. Below are a few of the advantages and disadvantages of buying a time share on the resale market. The 7-Minute Rule for How Much Does It Cost To Buy A Timeshare

In the majority of timeshare suites, you can anticipate to discover kitchen areas, washers/dryers, separate home, and much more. Cost. On the resale market, you can buy timeshare ownership for a fraction of the cost of timeshare on the main market. Value. In many cases all the benefits that are provided to retail timeshare buyers likewise transfer to resale buyers. Timeshares do not increase in worth like traditional property. Timeshare can be costly if you purchase on the main marketing or do not do your research (some programs have high yearly costs that make the cost of ownership less cost-effective). If your program is not part of Additional hints a club, you can get locked into vacationing in the exact same location each year. When you choose you wish to buy, you can search an excellent choice of timeshare resales on this site. We advise you do a little research on the brand/resort of your interest, and then proceed and see what's readily available that matches what you're searching for. You'll then make a deal, and negotiate from there with a licensed broker. Similarly, our certified genuine estate agents will be there to assist need to you want to sell your timeshare home. For more details, contact VacationOwnership. com's brokers by calling (866) 633-1030. You also have the option to lease your timeshare if you're simply aiming to cover expenditures and can't utilize your week in a given year, or of course you can search our existing leasings if you're looking to schedule a journey without dedication.

The last several years have ushered in numerous changes in the roles that sellers, buyers, and realty agents play in property sales and transactions. The number of for-sale-by-owner property listings now equal those which are handled by certified agents. Customer access to once-privileged information and the ease of utilizing online services has actually transformed the realty market, and it has revolutionized the timeshare industry also. How How To Buy A Timeshare Resale can Save You Time, Stress, and Money.

Though many consumers do not recognize it, purchasing, selling or renting timeshare often makes up a legal genuine estate transaction that is not only binding however frequently managed by law. When a timeshare residential or commercial property is owned by deed (deeded ownership), it is considered "real" property. As such, lots of property laws (though not all) are appropriate to timeshare owners in the very same way they are to homeowners. You deserve to cast a vote in all matters needing a vote of owners, including choosing a Board of Directors to govern the Association. The Board of Directors will normally hire a resort management business to run the resort. Some deceitful developers of undeeded resorts have "oversold" the job; i. ( This is more than likely to happen at an undeeded resort due to the fact that the lack of deeds linking units offered to specific ownership interests makes it much easier to oversell the resort.) When this happens, owners will find it really tough to schedule an usage period. Appropriately, if you are acquiring a week at an undeeded floating time resort, you should identify whether you are properly safeguarded versus overselling of the resort's inventory. A getaway club is a company that owns numerous timeshare homes in various locations. If you are a club member, you can book area at the numerous resorts that are part of the club in accordance with club guidelines. You pay yearly costs, and there is an initial cost to sign up with the trip club. Club subscriptions can usually be purchased, offered, or passed to successors. There can be different levels of membership, with some membership levels receiving greater top priority in booking specific units or having access to bigger units. In some cases memberships might be connected with a "house" resort, with club members receiving top priority in reserving space in read more their "home" resort. On the other hand, other holiday clubs are simply business that pre-sell holidays, and subscription in such clubs does not include any right in the governing of the club. Ownership of homes consisted of in a club is typically structured in one of two ways: The designer (or its successors) owns the residential or commercial properties, with the club having access to the residential or commercial properties by means of a contractual relationship with the owner. In this case, the homes would be owned by the club collectively and not by members separately. If your club membership also provides you a fractional ownership in the club, then you will own the properties indirectly through the club. In either case, if the club ceases operations, you can quickly lose your right to use the properties without compensation. Examine This Report about How Much Is A Timeshare In Disney

This arrangement offers some extra security to the club members if the club stops operations. Some trip clubs sell "deeded" subscriptions. If you own or are thinking about purchasing a "deeded" holiday club subscription, you ought to read your files to confirm what your deed represents. With some "deeded" vacation clubs, each membership includes a deed for ownership of a particular system and week at a resort. In other cases, the "deed" may represent a fractional ownership of the vacation club. In yet other clubs, the "deed" is just a certificate for subscription in the getaway club, without representing ownership of any real property. Trip clubs and right-to-use resort properties have lots of common features, and many of the warns formerly described for right-to-use jobs also apply to holiday clubs. In a common points program, you join the program by buying a subscription (how can i sell my timeshare). You then receive a defined number of points every year, with the variety of points you get established by the terms of the subscription you acquire. You can then exchange these points for lodgings at the resorts that take part in the points program. Similar to trip clubs, most points programs use several resorts in which you can reserve weeks. The variety of points needed to acquire accommodations will usually differ with the lodgings picked. Elements influencing the variety of points required for your requested lodgings include: The popularity of the resort The size of the accommodations The number of nights of tenancy The particular nights asked for (weekend and vacation nights normally require more points per night than do mid-week nights) The season of the year. The majority of points programs will allow you to collect points over 2 or more years, so that you can trade to a larger unit or more popular resort if you want to take a trip less frequently. Some points programs will also allow you to occupy a resort for less than a full week at a minimized variety of required points. I anticipate that other points programs will include comparable features in the future. I also anticipate that regular traveler programs operated by travel business such as airlines and hotel chains will establish tie-ins with timeshare points programs to additional extend point generation and redemption chances. Points programs can be connected to a deeded ownership or can be a direct "buy-in" not linked to ownership of a specific week. The 2-Minute Rule for How To Sell My Timeshare

Points programs can be run by a program operator, or can be part of a getaway club timesharing program - how to purchase a timeshare. Just recently, some exchange companies (see Lesson 3 for a discussion of exchange companies) have begun developing points programs. An essential worry about points programs is the long-lasting "value" of your points in reserving lodgings. If you own or are considering purchasing into a points system, you ought to inspect the program files carefully to identify what securities you might have against such losses in exchange power. Points programs and right-to-use resort properties have many typical features, and the majority of the cautions formerly explained for right-to-use projects also use to points programs. Through such exchanges, you can get timeshare lodgings in desirable trip areas throughout the world. Exchanging likewise allows you to getaway at different times of the year, even using a fixed week. The simplest exchange method is to discover a timeshare owner who is interested in exchanging his or her week for your week. Another exchange option occurs when your timeshare ownership is part of an exchange program that includes numerous resorts in various locations. In these plans, you can exchange your week for a week at another resort within the group. Lots of timeshare management business that operate resorts in different areas provide this type of exchange service as part of their management services. The most common exchange technique https://designlike.com/simple-ways-to-invest-in-real-estate/ is through a timeshare exchange business. To do this, you "deposit" your week with the exchange company. As other owners deposit their weeks (and as resorts deposit unsold weeks with the exchange company), the exchange business develops up an inventory of weeks that are readily available for exchanges. The exchange company thus serves as a clearinghouse for people making exchanges. Keep in mind that the owner of the week you exchange for will almost never ever be the individual who receives the week you transfer. The demand for lots of resorts differs seasonally. For example, for individuals living in the northern hemisphere, beach locations are popular in the summer season, whereas ski resorts are most popular during ski seasons. The Best Guide To How To Get Out Of A Timeshare Contract In Florida

This value affects both the rate of the system and the quality and types of exchanges you can make with the timeshare system. Resort Condominiums International (RCI) and Period International (II), the 2 largest exchange companies, both divide weeks into 3 seasons, designated by color. For RCI, the designations are: Red: high need season White: intermediate demand season Blue: low need season For II, the designations are: Red: high demand season Yellow: intermediate demand season Green: low demand season The classifications of seasons differ with each resort. With a routine life insurance coverage policy, your household can use the payout for the most pressing costs, whether it's home loan payments, other loans or college tuition. A term life insurance coverage policy can supply more bang for your buck than a mortgage life insurance coverage policy. A term policy allows you to pick the amount of coverage and policy length. In short, term life uses many of the advantages timeshare brokers of home loan defense insurance coverage but with lower premiums, more flexibility and more control. Homeowners insurance provides coverage in case your home is damaged or damaged, and likewise supplies liability for injuries sustained by visitors to your residential or commercial property. In addition, the loss or damage of residential or commercial property in and around the dwelling is covered as well (the contents). The quantity of money your house is guaranteed for is called the house limitation coverage. While house owners insurance may be optional if you own your home free and clearMost mortgage loan providers need a particular quantity of coverage if you bring a house loanThis secures their financial interest in your propertyBecause keep in mind, they let you fund a large chunk of itMost banks and lenders require that homeowners buy enough insurance coverage to cover the amount of their home loan. However you should also ensure that your property owners insurance coverage covers the expense of reconstructing your property in case of severe damage. Your house is probably your greatest liability, and for many its likewise their savings, so complete coverage is a must. Homes and other structures on your residential or commercial property Personal residential or commercial property Personal liability Earthquake insurance coverage Flood insurance coverage Personal valuables beyond your protection limitations (think expensive jewelry)Damages triggered by severe weather such as wind, lightning, hail, and fire are normally covered. However, natural events such as earthquakes and floods require separate insurance. Additionally, understand your policy limitations because costly products aren't automatically covered (think fashion jewelry), and might need their own prolonged coverage. Understanding the cost to rebuild your house is among the most important and misconstrued elements of homeowners insurance coverage. The Best Strategy To Use For How Do Adjustable Rate Mortgages React To Rising Rates

However in reality, the worth of your house might be less than (or more than) the actual cost to rebuild it from the ground up. And building costs may increase as residential or commercial property worths fall, so it's important to evaluate the cost of a total restore. Style of your house Variety of spaces Square footage Local building and construction costs Other structures on your residential or commercial property Special featuresDo note that if you make any considerable enhancements to your home, you need to also increase your coverage in the event that you require to restore. Make certain they are guaranteed for replacement expense and not ACV, or real money worth, which is the depreciated value. Set your policy to upgrade each year based on inflation and rising building expenses, and ensure that your policy covers living expenses while your house is being fixed if the damage is too extreme to remain in your home during building. Many customers merely take whatever policy is tossed at them, or worse, buy the minimum needed by their bank or lending institution. For many house owners it's merely a stipulation or requirement to get the offer done, much like cars and truck insurance, but failure to insure your greatest asset/liability correctly might be the greatest mistake of your life. mortgage insurance. Prior to producing this blog site, Colin worked as an account executive for a wholesale home loan lender in Los Angeles. He has actually been composing passionately about home loans for nearly 15 years. Home loan life insurance coverage is a kind of insurance particularly created to secure a repayment mortgage. If the policyholder were to pass away while the mortgage life insurance was in force, the policy would pay a capital amount that will be simply adequate to repay the outstanding home loan. Home mortgage life insurance coverage is supposed to secure the customer's capability to pay back the mortgage for the lifetime of the home mortgage. When the insurance starts, the worth of the insurance protection need to equate to the capital exceptional on the repayment mortgage and the policy's termination date must be the exact same as the date scheduled for the last payment on the payment mortgage. The insurer then computes the yearly rate at which the insurance protection ought to reduce in order to mirror the worth of the capital outstanding on the payment home mortgage (after my second mortgages 6 month grace period then what). About What Is The Percentage Of People Who Pay Off Mortgages

Some home mortgage life insurance policies will likewise pay if the insurance policy holder is identified with a terminal disease from which the insurance policy holder is expected to die within 12 months of medical diagnosis. Insurance provider sometimes include other functions into their home loan life insurance coverage policies to reflect conditions in their nation's domestic insurance market and their domestic tax guidelines. In many cases, standard life insurance coverage (whether term or long-term) can provide a better level of security for significantly smaller sized premiums. The greatest benefit of traditional life insurance over home mortgage life insurance coverage is that the former maintains its stated value throughout the life time of the policy, whereas the latter guarantees to pay out a quantity equal to the client's impressive home mortgage debt at any time, which is naturally a decreasing amount. In addition, providing banks typically incentivise customers to acquire home mortgage life insurance coverage in addition to their new home mortgage by means that are on the verge of connected selling practices. Tied selling of an item of self or of an affiliated celebration, nevertheless, is prohibited in most jurisdictions. In Canada, for instance, this practice is explicitly forbidden by Section 459. Finally, home loan life insurance is not needed by law. It depends on the client-borrower whether he or she will choose to protect his/her property financial investment by an insurance product or not. Similarly, the choice of insurance company is completely unrestrained also. Due to the fact that of these suboptimal qualities of mortgage life insurance coverage, the item has actually gone through sharp criticism by financial specialists and by the media across North America for over a years. Nevertheless, lots of critics fail to consider that in a lot of cases where term life insurance coverage is denied for health reasons, home mortgage life insurance is still available (this does not guarantee that you are covered, however rather you're enabled to pay the premium of the insurance coverage, the financial institution holds the right to reject the claim. When it comes to home loan life insurance coverage, this can be an excellent advantage for your heirs and enjoyed ones. On the other hand, you can do much the very same thing with term insurance coverage while naming your own beneficiaries. It pays to go shopping for the very best kind of life insurance coverage to cover your home loan expenses in the event of your death. Learn how to create tax-efficient earnings, prevent mistakes, decrease threat and more. With our courses, you will have the tools and understanding needed to achieve your financial objectives.

All about Why Do Banks Make So Much From Mortgages

Whether you're a novice house purchaser or you're experienced in genuine estate transactions, the procedure of finding, exploring and negotiating for your brand-new home is amazing. But once you've found a new place you'll have some documents to handle. Navigating that documentation together with all of the requirements during a home sale can be confusing, especially when it concerns your home loan and your homeowners insurance coverage. Let's break down the basics. When you purchase a house, there are 2 types of insurance that'll come into play: house owners insurance and personal home loan insurance coverage (PMI). We'll specify both to give you a clearer image of what your insurance commitments are as a property owner. Let's begin with homeowner's insurance coverage: is the insurance policy you're going to You can find out more count on if something occurs to your home, your personal effects and/or visitors on your residential or commercial property (what are the interest rates on 30 year mortgages today). But the primary purpose of your property owners insurance is to satisfy your specific, unique needs. Of course, it offers the home and liability defense you 'd anticipate from a superior policy but at American Family, you can tailor your policy with a wide array of add-on coverages. Ask your American Household representative about insurance coverage recommendations and conserving money by bundling and making the most of discount rates. Rather, PMI is how home mortgage lenders protect themselves from borrowers who stop paying, default and foreclose on their homes. PMI is normally required for borrowers who can't make a deposit on the home of 20 percent or more. However after you've paid down a minimum of 20 percent of your home loan's principal, you should ask your lending institution to eliminate the PMI. If you spend for your homeowners insurance as part of your home loan, you have an escrow. An escrow is a different account where your loan provider will take your payments for property owners insurance coverage (and in some cases real estate tax), which is constructed into your home mortgage, and makes the payments for you. This is beneficial for both you and your loan provider you do not have to fret about keeping an eye on one or 2 more bills, and they're ensured that you're remaining current on those monetary spg timeshare responsibilities. Like your PMI, if you haven't paid a 20 percent or more deposit on the home, possibilities are that your loan provider will need it. If you've made a deposit of 20 percent or more, you can normally choose whether you wish to pay your insurance coverage with your mortgage. The smart Trick of Which Congress Was Responsible For Deregulating Bank Mortgages That Nobody is Talking About