|

In other words, you require to prove that the funds in fact came from https://dominickkrys529.skyrock.com/3341946254-Get-This-Report-on-Who-Issues-Ptd-s-And-Ptf-s-Mortgages.html the donor in concern by paper routing the cash. Otherwise, the loan provider might question the source. After all, you might state you got a present however truly just took out an unsecured loan or a charge card cash loan. For the record, it's also possible to receive gift money as a wedding gift and after that apply it to your mortgage. Nevertheless, you'll require to furnish a copy of your marriage license, confirm the funds in your account, and reveal that the cash was deposited into your account within 60 days of the special day. But like whatever else, you need to be diligent and ensure you please all the conditions connected to the present funds to make sure everything runs efficiently.(image: Lots of Fantastic Artists). If you're imagining homeownership but having a hard time to save sufficient cash for your down payment, you're not alone. The median home in the United States costs $217,600 in 2018, according to the US Census Bureau. A 20% deposit for a home that price would be a cool $43,520. If you don't have that type of money on hand, the response to homeownership may be a money present together with a mortgage present letter. What Are The Current Refinance Rates For Mortgages Things To Know Before You Buy

However, the gift-giver will require to provide a present letter that you can provide to your lending institution to prove that the funds are formally and legally yours. A gift letter for a home mortgage is a letter to your lender from the individual who gifted you the cash specifying that the tug timeshare cash is a gift that does not require to be paid back. Usually, a present letter consists of: Your donor's name, address, and phone numberThe donor's relationship to you (moms and dad, grandparent, etc)The precise talented quantity, and a complete sentence stating that you as the borrower don't owe the donor anything for the moneyThe date the present quantity was transferredThe address of the residential or commercial property that the home loan is forSignatures from you and the donorIt's important to keep in mind that you can not, under any circumstances, pay back a gift for a down payment. It's also essential to keep in mind that presents over the amount of $15,000 from one person to another will be qualified to be taxed. For example, your mother can present you $15,000 and your daddy can present you $15,000 and they will not pay the gift tax on either gift. However if your mother provides you $15,001, she will have to pay the present tax on that $1. The donor always sustains the tax obligation. These annual tax exemption rates alter year over year, so make sure to inspect the rates before anyone provides you a cash present. As soon as the letter has actually been written, you must provide it to your lending institution as a part of your overall application documents.

Not known Facts About What Are Interest Rates Today On Mortgages

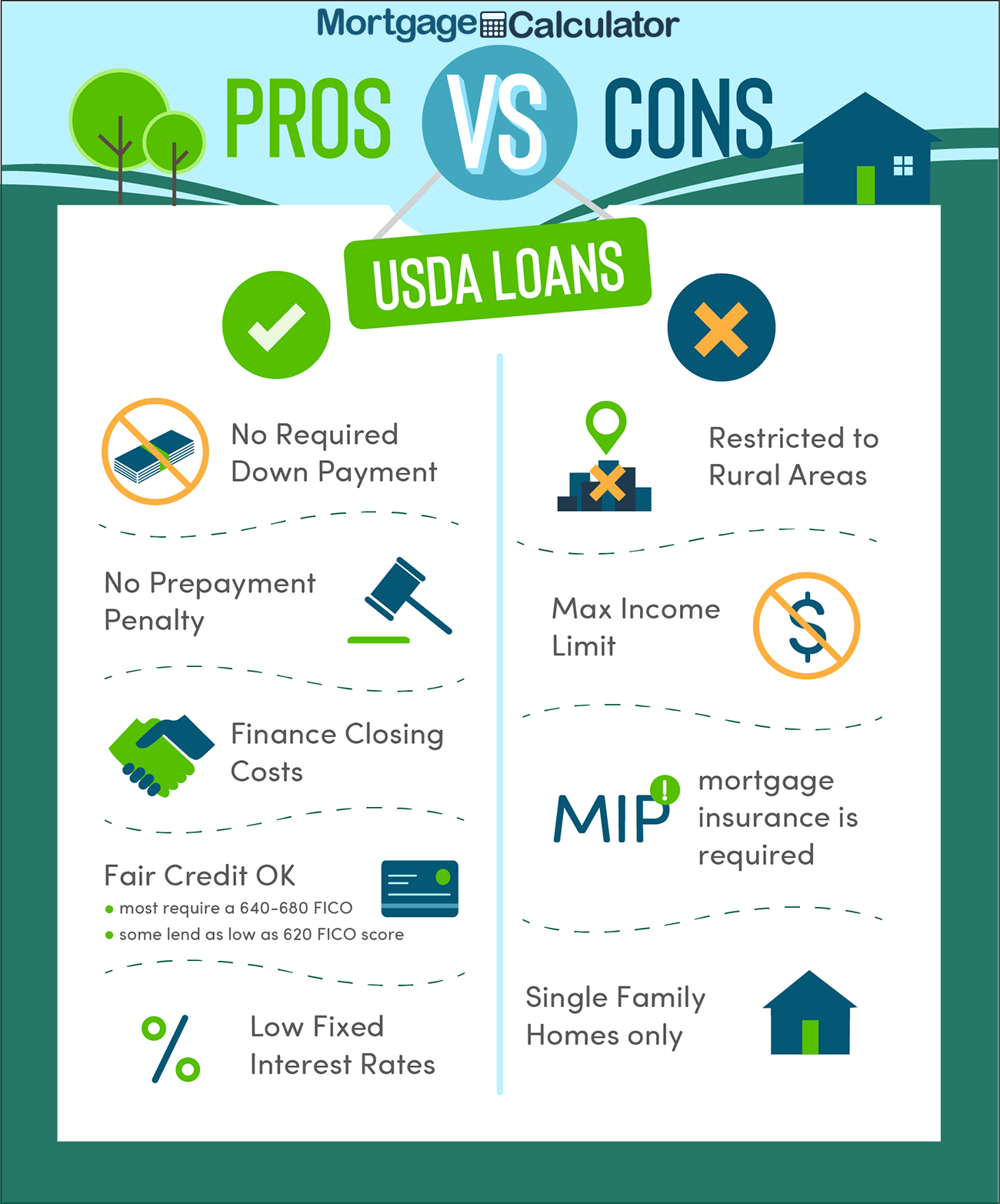

The letter ought to be included with other financial info, like your list of possessions, your income, and your work history and existing work status. Your loan provider will evaluate all your documents, consisting of the letter. Lenders might request extra bank statements from your present giver, to ensure that they have the money to provide which that the cash was moved on the date specified in the letter. Different types of loans have their own rules to receive them. who has the best interest rates on mortgages. With VA, USDA and FHA home mortgage, the present cash can come from anyone who doesn't have an ownership stake in the residential or commercial property that's being bought. The cash can originate from a friend, any member of the family, your employer or even an authorized not-for-profit firm or charity. The cash can likewise originate from a fianc or domestic partner. The cash can't originate from anybody with any stake in your home, or who is associated in any method with somebody who becomes part of the transaction, like the property representative or the contractor. If you're utilizing a standard loan from Fannie Mae, you can timeshare foreclosure utilize a present letter for your individual or secondary house, but you can't use a present letter on a standard loan for a financial investment property. Loans from the Veterans Affairs office are qualified for a present letter. The gift can be utilized to cover both closing expenses and the down payment. An FHA loan enables both the deposit and closing costs to be paid for by a gift. Gifts for a USDA loan can be supplied from "an organization or another person not residing in your home" and require both a gift letter and for the candidate to submit Kind RD 3550-2. All about What Is The Current Index For Adjustable Rate Mortgages

If you wish to utilize a monetary gift for your deposit, your next steps need to be to ask the individual offering you the cash to write a present letter. You may likewise consider keeping the present money in a different checking account, both to keep your financial resources arranged and to maintain that cash for your real home purchase. If you're like among numerous Australians, you might have asked your parents to gift you the money for your deposit. With some loan providers, a talented deposit methods you do not need to prove authentic cost savings and essentially get into the home market with no deposit. The trick to getting approved is utilizing a present letter design template that the bank will accept as proof that the cash from your moms and dads is non-refundable. Lenders require to validate the source of a borrower's deposit to make sure they are not obtaining the deposit off credit cards or a personal loan. Some Australian lenders won't provide to people who have gotten their deposit as a present. Please read our page about mortgage with a talented deposit to learn more about the loan alternatives offered to you. If your loan provider has actually particularly requested for a statutory statement then please utilize the 2nd template. 1/10/2018 To Whom It May Issue: Re: John Smith I verify that I am providing my child John Smith a genuine present of $50,000 for him to utilize to purchase a residential or commercial property - why reverse mortgages are a bad idea. This gift is not repayable or refundable. What Are The Current Interest Rates On Mortgages Things To Know Before You Buy

Regards, (SIGN) Adam Smith1 George St Sydney NSW 2000 If a Home Loan Specialists mortgage broker is arranging your home mortgage, please email your signed letter through to them. Which loan providers will accept a gifted deposit? Call us on or enquire online to discover. Utilize this home loan gift letter design template if your lending institution has particularly requested a statutory statement. If you're not sure what design template to use, please call us on to discuss. Statutory Statement I/We: Adam Smith Of: 1 George St Sydney in the State of New South Wales, do solemnly and all the best state as follows: I will give my boy John Smith a total of $50,000 to help him to acquire a residential or commercial property.

0 Comments

If a borrower is missing from their main home for longer than 12 months or has completely moved from their main home, then the loan servicer must look for approval from HUD to call the reverse home mortgage due and payable. Once approval is acquired, the servicer sends by mail a need letter to the borrowers requiring them to either pay back the loan completely or treat the loan default by re-occupying the residential or commercial property as their primary home. If anybody co-signed for the house loan, that person would be accountable for settling the debtwhether or not they reside in the house or have an ownership interest. Non-owner co-signers are probably most at-risk in regards to being accountable for paying your outstanding home mortgage financial obligation after you die. Sometimes, successors might not be able to take over the home loan.

If the house is worth more than is owed on it, the difference can go to your heirs. Your administrator can sell the home and utilize the profits to settle other financial obligations or disperse assets to heirs. Additionally, if a Great post to read specific successor takes control of the home loan and ownership of the house, that person can pocket the distinction. If all else stops working, the loan provider can simply foreclose, and your loved ones won't be accountable for the debtas long as they didn't co-sign on the mortgage. Reverse home mortgages are various due to the fact that you don't make month-to-month payments. House Equity Conversion Home Mortgages (HECMs) are the most typical kinds of these kinds of loans, which must be settled after the last customer (or qualified spouse) passes away or vacates. If they wish to keep the house, they'll have 1 month to pay off the full loan balance or 95% of the home's appraised valuewhichever is less. If they desire to offer the house, then the lending institution will take the profits as payment for the loan. Some fundamental estate preparation will make things much easier for everyone. Not known Details About Why Is There A Tax On Mortgages In Florida?

The quicker, the better. A simple will might work, or you can utilize additional techniques (when did subprime mortgages start in 2005). Life insurance coverage may provide a fast money injection to assist your successors settle your home mortgage or stay up to date with month-to-month payments. That money can give everybody alternatives, including an enduring spouse who may or might not desire to keep the home. With the assistance of certified experts, examine whether or not it makes sense to hold your realty in a trust or a service entity like an LLC. Adding extra owners to the title could also be an option. Any action that keeps your house out of probate can assist to minimize costs and smooth the transition for your beneficiaries. Specifically if your member of the family will have a hard time making payments after your death, make funds readily available to them. This will assist them lessen tension and paperwork, and they can offer the house for a fair rate if that's what needs to happen. In the meantime, They'll require to pay the mortgage, maintain the property, and remain existing on taxes. It's not enjoyable, and it's more difficult for some than others, however communication can go a long method towards preventing distress when the unavoidable happens. Learn if liked ones wish to keep the house, or if they 'd choose to proceed. If you have numerous successors, clarify who gets whatand under what conditions. Some Ideas on Which Mortgages Have The Hifhest Right To Payment' You Need To Know

A reverse home loan is a type of home mortgage loan that's secured against a residential property that can provide senior citizens added income by providing access to the unencumbered worth of their properties. However there are disadvantages to this technique, such as significant fees and high-interest rates that can cannibalize a substantial portion of a homeowner's equity. While a reverse home loan may be ideal for some situations, it is not constantly finest for others. If you wish to leave your home to your kids, having a reverse mortgage on the property could trigger issues if your successors do not have the funds needed to pay off the loan (when did subprime mortgages start in 2005). When property owners pass away, their partners or their estates would usually pay back the loan. According to the Federal Trade Commission, this typically entails selling the home in order to produce the needed cash. If the house costs more than the exceptional loan balance, the leftover funds go to one's beneficiaries. That is why customers must pay home loan insurance coverage premiums on reverse house loans. Getting a reverse mortgage could complicate matters if you want to leave your home to your kids, who may not have the funds required to settle the loan. While a traditional fixed-rate forward home mortgage can provide your heirs a financing service to protecting ownership, they may not qualify for this loan, in which case, a cherished family house might be sold to a stranger, in order to rapidly please the reverse mortgage financial obligation. How Reverse Mortgages Work In Maryland Can Be Fun For Everyone

Those boarders may likewise be forced to abandon the house if you vacate for more than a year since reverse home loans need customers to reside in the home, which is considered their primary home. If a borrower dies, offers their home, or vacates, the loan right away becomes due. Senior citizens plagued with health problems may obtain reverse home mortgages as a method to raise money for medical expenses. However, they need to be healthy sufficient to continue house within the home. If a person's health declines to the point where they must transfer to a treatment facility, the loan should be repaid in full, as the house no longer qualifies as the customer's main house. For this factor, debtors are needed to accredit in writing each year that they still live in the house they're borrowing versus, in order to prevent foreclosure - when does bay county property appraiser mortgages. If you're pondering moving for health issues or other reasons, a reverse mortgage is probably unwise because in the short-run, http://louisyxjc597.timeforchangecounselling.com/what-is-the-highest-interest-rate-for-mortgages-fundamentals-explained steep up-front costs make such loans economically impractical. k.a. settlement) costs, such timeshare wyndham as residential or commercial property title insurance, home appraisal fees, and examination costs. Homeowners who unexpectedly leave or offer the home have simply 6 months to repay the loan. And while debtors might pocket any sales earnings above the balance owed on the loan, countless dollars in reverse home loan expenses will have already been paid out. 3 Easy Facts About What Type Of Insurance Covers Mortgages Explained

Failure to remain existing in any of these locations might cause loan providers to call the reverse home mortgage due, possibly resulting in the loss of one's home. On the bright side, some localities provide real estate tax deferral programs to assist elders with their cash-flow, and some cities have actually programs geared towards helping low-income senior citizens with home repair work, however no such programs exist for property owner's insurance coverage. The smart Trick of What Is The Highest Interest Rate For Mortgages That Nobody is Talking About5/12/2021 Go figure. The situation is a lot more complex, so consider this is an initial lesson on a really complex subject. Tip: Mortgage rates can rise really rapidly, however are frequently reduced in a sluggish, calculated manner to safeguard home loan lenders from fast market shifts (how does chapter 13 work with mortgages). That extremely low marketed home mortgage rate sure appearances goodBut make sure to take a look at the great printYou most likely need to be an A+ borrowerAnd you might need to pay discount rate points tooAlso note that the par rate you see advertised on TV and the web frequently don't take into account any home loan rates changes or charges that might drive your real interest up considerably. If your deposit or credit rating isn't that high, or your house equity is low, your home loan rate might sneak higher as well. Occupancy and home type will likewise drive rates higher, presuming it's a second home, investment residential or commercial property, and/or a multi-unit property (why do banks sell mortgages to other banks). So expect to pay more if that holds true.

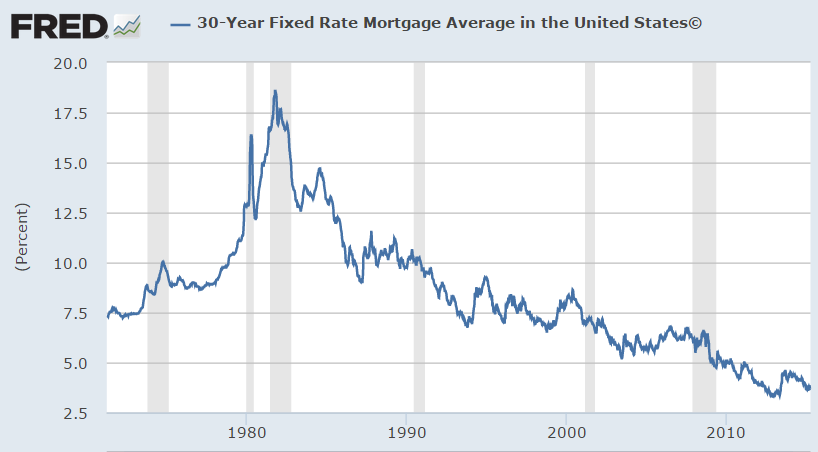

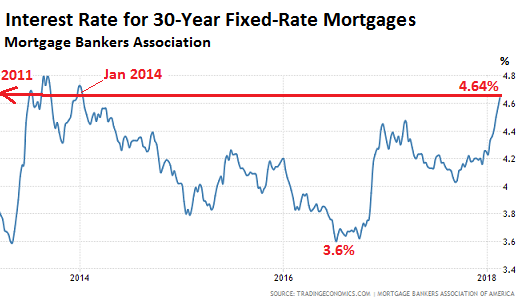

There are also loan amount restrictionspricing can alter depending on if the home mortgage is adhering or jumbo. Typically, monthly payments are greater on the latter, all else being equal. In other words, YOU and your property matter too. A lot!If you're a dangerous debtor, at least in the eyes of potential home loan lending institutions, your home loan rate might not be as low as what you see promoted. At the customer level, the greatest aspect in identifying the cost of a mortgage is usually credit report. Among the most important aspects that you can control is your credit rating, so if you can at least get a manage on that and work to keep your scores above 760, your pricing must be optimum, all else being equal. There are loan calculators that will inform if paying points make sense depending upon your circumstance, how long you plan to stay in the home, and so on. Rates can also differ substantially based upon just how much a specific lender charges to stem your loan. So the final rate can be manipulated by both you and your lender, regardless of what the going rate happens to be. Last but not least, note that there are a range of various loan programs available with different interest rates. Are we talking about a 30-year fixed rate or a variable-rate mortgage, the latter of which will have a lower rates of interest. Loan type and loan quantities can play a big role here. Below are Freddie Mac's, upgraded weekly every Thursday morning. Not known Details About What Credit Score Model Is Used For Mortgages

The data is collected Monday through Wednesday, so they aren't necessarily going to compare with today's home loan rates if rates increased or fell from then until now. Consider this a starting point:30- Year Fixed * 2. 71% 2. 71% 3. 73% 15-Year Set * 2. 26% 2. 26% 3. 19% 5/1 ARM2. 79% 2. 86% 3. 36%- Home mortgage rates are currently trending -* symbolizes a record lowSince 1971, Freddie Mac has actually performed a weekly survey of consumer home loan rates. These averages don't use to government mortgage like VA loans or an FHA home mortgage. The numbers are based upon quotes used to "prime" customers, those with high credit scores, meaning best-case pricing for the most part. I think the property key in the study is for a one-unit primary residence as well, so anticipate a rate increase if it's a villa or rental residential or commercial property, or multi-unit property. To put it simply, your mortgage rate might deviate from the national average for any variety of factors, however if your home mortgage is pretty run of the mill, you may anticipate pricing to be comparable. As you can see, 30-year set mortgage rates are the most pricey relative to the 15-year repaired and select variable-rate mortgages. So you pay a premium for the stability and lack of threat, and the opportunity to refinance if rates occur to go down. http://louisyxjc597.timeforchangecounselling.com/how-in-what-instances-is-there-a-million-dollar-deduction-oon-reverse-mortgages-can-save-you-time-stress-and-money Rates on the 15-year fixed are considerably cheaper, however you get half the time to pay it off, indicating larger monthly payments and a lot less interest paid. 25%) listed below the 30-year repaired. The shorter term suggests you'll also save a ton on interest. Rates on ARMs are discounted at the outset since you only get a limited set period before they become adjustable, at which point they normally increase. Grab a mortgage calculator and cost out various loan types to see what makes one of the most sense for your situation. If your particular loan circumstance is higher risk, whether it's a greater LTV and/or a lower credit score, it will probably be priced higher. If you're looking for existing mortgage rates of interest, you can take a look at these weekly averages to see both the direction of rates and the ballpark figures to at least get an estimate of what you might get at any provided time. 3 Simple Techniques For How Many Mortgages Can One Person Have

71% per Freddie MacPreviously it had been as low as 2. 72% during the week ended November 25th, 2020The 15-year fixed also struck its all-time low of 2. 26% on December 3rd, 2020During the week ending December 3rd, 2020, 30-year fixed mortgage rates hit brand-new all-time lows. The popular 30-year fixed fell to 2.

72%, per Freddie Mac, the most affordable point because tracking started all the way back in 1971. Formerly, it had been as low as 2. 72% during the week ended November 25th, 2020. So far, there have actually been 14 new record lows set for mortgage Additional hints rates in 2020. The 15-year set hit a record low of 2. It had previously been as low as 2. 28% throughout the week ended November 25th, 2020. Its lowest point was 2. 56% during the week ended May 2nd, 2013 prior to reaching these current new lowest levels a number of times in 2020. During the very same week back in 2013, the $15/1 ARM likewise strike its all-time record low of 2. Lastly, the one-year ARM fell to 2. 41% during the week ended April 10, 2014, its lowest point on record given that 1984. The majority of economic experts don't see rates falling back to these lows again, though anything is possible if the economy warrants such a relocation. Spoiler alert, rates hit new lows!Wondering if mortgage rates are going up or down in 2020 and the year after? Wonder no longer. Take them with a grain of salt due to the fact that they're not always accurate, simply forecasts for future rate motion. Fannie Mae3. 6% 3. 6% 3. 6% 3. 5% 3. 6% Freddie Mac3. 8% 3. 8% 3. 8% 3. 8% 3. 8% MBA3. 7% 3. 7% 3. 7% 3. 7% 3. 8% NAR3. 7% 3. 7% 3. 8% 3. 8% 4. 0% As you can see, home mortgage rates are predicted to stay low in 2020. Obviously, it will vary a little depending on which anticipate you think. Home mortgage rates are expected to remain in the mid-to-high 3% realm in 2020, which need to be welcome news to many. I have simply launched 2020 mortgage rate forecasts for those searching for a more comprehensive evaluation. Check out more: What home loan rate can I expect!. Some Ideas on How Do Reverse Mortgages Work After Death You Need To what happens to my timeshare if i die Know

?.!?. NOTICE: This is not a dedication to provide or extend credit. Conditions and limitations might use. All home loaning items, consisting of mortgage, home equity loans and home equity lines of credit, are subject to credit and collateral approval. Not all house financing items are offered in all states. Risk insurance and, if applicable, flood insurance are needed on collateral residential or commercial property. With the proper documents, you may have up to a year to offer the house before it need to be turned over. If you stop working to offer the proper paperwork, the loan servicer may start foreclosure procedures within 6 months. Here are a couple of things you require to understand prior to inheriting a reverse home mortgage after the death of the borrower. how much is mortgage tax in nyc for mortgages over 500000:oo. A lot of reverse home mortgages are house equity conversion home loans (HECMs), which are subject to FHA guidelines. Non-HECMs might not follow these very same rules. Talk with a home mortgage expert, accountant, and other trusted consultants to help you understand the ins and outs of a reverse mortgage. Communicate with the loan servicer. After the death of the debtor, keeping in excellent communication with the loan servicer is essential to ensure a smooth transition. If the loan amount is less than the home deserves, then offering the property might make the a lot of sense. Here are some suggestions when selling a home with a reverse home loan. Non-recourse. A reverse home loan is a non-recourse loan. This indicates customers are never responsible for more than 95% of the house's evaluated worth - what were the regulatory consequences of bundling mortgages.

Avoiding negative financial effect. You might avoid the obligation of paying the loan quantity, including the unfavorable monetary impact of the loan quantity exceeding the house's value, by finishing a deed-in-lieu of foreclosure, short sale, or by walking away from the home. This will permit the loan servicer to begin foreclosure proceedings. The 9-Second Trick For What Percentage Of Mortgages Are Below $700.00 Per Month In The United States

As soon as you have actually decided to offer the residential or commercial property, or settle the loan, you have six months from the death of the borrower to complete the deal. After this time, the loan servicer may proceed with foreclosure. Time extensions. Helpful resources If you need extra time to market and offer the home prior to foreclosure procedures take place, you may request approximately 2 90-day extensions. Avoiding foreclosure. If you do not react to the due and payable notification, if the home does not sell before your extension ends, or the real estate tax and insurance coverage are not paid, then the loan servicer may begin foreclosure. Work closely with your loan servicer to guarantee all documentation is completed effectively to prevent early foreclosure. Over the last 2 decades, lots of believed reverse home loans ought to just be used for the desperate and as a last option. who took over abn amro mortgages. I personally remember when reverse mortgages were being advertised on TELEVISION commercials with substantial Hollywood stars promoting about how fantastic they were. The generation that withstood the great anxiety was quickly marked the concept as too great to be true. There has actually been favorable press around reverse home loans. Popular monetary advisers are now including the House Equity Conversion Mortgage (HECM) to the wealth management tool kit. It's normally concurred that the FHA and HUD have fixed lots of major problems with the HECM program. With all this brand-new awareness, there still appears to be unpredictability and concern about what occurs at the end of a reverse home loan, i. The smart Trick of What Percentage Of National Retail Mortgage Production Is Fha Insured Mortgages That Nobody is Discussing

when it comes time to pay it back. So that brings us to the function of this short article. We will be analyzing the last days of the maturity on a reverse mortgage when it comes due, what takes place after the borrower dies, how the borrower's successors play into everything, and how you settle the loan. However, there are others, and a better suited heading might've been "What Happens When a Maturity Event Happens?" The house owner passing away is just one of several maturity events. Here are the others that are common: Property is sold House owner indications the title away Property owner lives in other places 12 months or more Taxes & insurance coverage are not paid in a prompt way (though the brand-new monetary assessment mainly fixed this concern) The home is not correctly looked after and maintained Let's proceed and look at the procedure that is set off by a maturity occasion: Maturity Occasion Occurs One of the formerly discussed occasions take place The lending institution creates a 'Demand Letter' The servicer mails an acknowledgement and need letter, to either the homeowner or his/her property owner's estate. The Estate Sends Out an Intent to Please File (within 1 month of the Demand Letter) Appraisal At the same time the loan provider orders an appraisal of the propertyThe estate settles the debt by paying the balance or The estate submits a demand for a 90 day extension or the loan provider lists the residential or commercial property for Sale The estate can submit a second 90 day extension Pre-Foreclosure notification When the extensions have actually ended or the estate has actually not responded and, if the property has not sold, the lending institution will issue a "Pre-Foreclosure" notification Foreclosure As this point the property is foreclosed on. The eliminate indicate borrowers on a reverse mortgage is to keep your family notified of the duties associated with a maturity event. The beneficiaries benefit by contacting the servicer as soon as possible after a maturity occasion. The house's equity sans the loan balance are an http://louisthka851.image-perth.org/little-known-facts-about-what-kinds-of-laws-prevented-creditors-from-foreclosing-on-mortgages asset and ought to be safeguarded. Some Known Questions About What Is The Best Rate For Mortgages.

This is not a legacy that a matriarch or patriarch dreams to leave. I understand of one family that a matriarch knew that her death was impending and her reverse loan would come due. She and her oldest daughter created an action package; it had the letters all pre-written and even stamped. This made everybody's life simpler, and we might all gain from this type of proactive organization. Open and keep an interaction loop between the loan provider, the house owners, and the beneficiaries. No one take advantage of a foreclosure on a residential or commercial property with a reverse home loan not the lender, not the FHA who guarantees the loan, and definitely not the borrower. Foreclosing is expensive in both time and money, and it makes the lender look bad. Nevertheless, the HECM program does need foreclosure under particular situations. A word of caution: the beneficiaries of a departed reverse mortgage debtor will not be successful in concealing that death. Dishonest successors who think otherwise beware. It likewise may cause time out to this thinking once it is comprehended that the 1 month to reply with an "intent to please" letter does not start at discovery. The 1 month time period starts at the time of death. An attempt at hiding a maturity occasion simply wastes important time. Some Known Details About What Are The Types Of Reverse Mortgages

However, if you want to put in the research you can comprehend how this loan works, and the maturity & payoff process is no different. The bottom line is that this special financial item is a practical choice for house owners to use in accomplishing their financial objectives. That said, the reverse home mortgage market is fluid and continuously changing - how did clinton allow blacks to get mortgages easier. Your best bet is to talk with intervals international timeshare a licensed reverse mortgage loan provider for updated guidelines and with any questions you might have. What occurs to your home loan after you pass away, and what can you do to make things easier for liked ones? The good news is that successors are not responsible for loans that they have nothing to do with, and you can prepare ahead to keep everyone in the homeif that's what they want. The Financial Crisis Inquiry Commission found that in 2008, GSE loans had a delinquency rate of 6. 2 percent, due to their standard underwriting and qualification requirements, compared to 28. 3 percent for non-GSE or personal label loans, which do not have these requirements. Additionally, it is unlikely that the GSEs' enduring budget-friendly housing objectives encouraged lenders to increase subprime loaning. The objectives came from the Housing and Community Development Act of 1992, which passed with frustrating bipartisan support. In spite of the fairly broad mandate of the budget-friendly housing goals, there is little evidence that directing credit towards debtors from underserved neighborhoods caused the real estate crisis. The program did not significantly alter broad patterns of home loan loaning in underserviced neighborhoods, and it functioned quite well for more than a decade before the private market started to greatly market riskier home mortgage products. As Wall Street's share of the securitization market grew in the mid-2000s, Fannie Mae and Freddie Mac's earnings dropped significantly. Figured out to keep bluegreen timeshare cancellation shareholders from panicking, they filled their own financial investment portfolios with risky mortgage-backed securities bought from Wall Street, which produced higher returns for their investors. In the years preceding the crisis, they also began to lower credit quality standards for the loans they acquired and guaranteed, as they tried to complete for market share with other personal market individuals. These loans were typically stemmed with large down payments however with little paperwork. While these Alt-A home mortgages represented a little share of GSE-backed mortgagesabout 12 percentthey were accountable for in between 40 percent and 50 percent of GSE credit losses during 2008 and 2009. These errors integrated to drive the GSEs to near personal bankruptcy and landed them in conservatorship, where they stay todaynearly a years later on. And, as described above, overall, GSE backed loans carried out better than non-GSE loans throughout the crisis. The Neighborhood Reinvestment Act, or CRA, is designed to attend to the long history of prejudiced loaning and motivate banks to assist satisfy the needs of all borrowers in all sectors of their communities, specifically low- and moderate-income populations.

Facts About How Does The Trump Tax Plan Affect Housing Mortgages Uncovered

The main concept of the CRA is to incentivize and support practical private lending to underserved communities in order to promote homeownership and other neighborhood financial investments - what are the main types of mortgages. The law has been modified a variety of times since its initial passage and has actually ended up being a cornerstone of federal neighborhood advancement policy. The CRA has facilitated more than $1. Conservative critics have actually argued that the requirement to meet CRA requirements pressed lending institutions to loosen their loaning requirements leading up to the housing crisis, successfully incentivizing the extension of credit to undeserved debtors and fueling an unsustainable housing bubble. Yet, the evidence does not support this narrative. From 2004 to 2007, banks covered by the CRA originated less than 36 percent of all subprime mortgages, as nonbank lending institutions were doing most subprime financing.

In overall, the Financial Crisis Query Commission determined that just 6 percent of high-cost loans, a proxy for subprime loans to low-income borrowers, had any connection with the CRA at all, far listed below a threshold that would indicate substantial causation in the housing crisis. This is because non-CRA, nonbank lending institutions were often the culprits in a few of the most unsafe subprime financing in the lead-up to the crisis. This remains in keeping with the act's relatively restricted scope and its core function of promoting access to credit for certifying, traditionally underserved borrowers. Gutting or eliminating the CRA for its expected role in the crisis would not only pursue the incorrect target however likewise held up efforts to reduce prejudiced home loan loaning. Federal real estate policy promoting price, liquidity, and gain access to is not some inexpedient experiment but rather an action to market failures that shattered the real estate market in the 1930s, and it has actually sustained high rates of homeownership since. With federal support, far greater numbers of Americans have taken pleasure in the benefits of homeownership than did under the complimentary market environment before the Great Anxiety. The smart Trick of What Kind Of Mortgages Do I Need To Buy Rental Properties? That Nobody is Talking About

Rather than focusing on the danger of federal government support for home loan markets, policymakers would be much better served analyzing what the majority of specialists have actually determined were causes of the crisispredatory loaning and poor guideline of the monetary sector. Positioning the blame on housing policy does not speak with the facts and threats reversing the clock to a time when most Americans might not even imagine owning a house. Sarah Edelman is the Director of Real Estate Policy at the Center. The authors want to thank Julia Gordon and Barry Zigas for their useful remarks. Any mistakes in this quick are the sole duty of the authors. by Yuliya Demyanyk and Kent Cherny in Federal Reserve Bank of Cleveland Economic Trends, August 2009 As increasing house foreclosures and delinquencies continue to undermine a monetary and financial recovery, an increasing quantity of attention is being paid to another corner of the home market: commercial genuine estate. This post discusses bank exposure to the business realty market. Gramlich in Federal Reserve Bank of Kansas City Economic Evaluation, September 2007 Booms and busts have played a prominent function in American economic history. In the 19th century, the United States took advantage of the canal boom, the railroad boom, the minerals boom, and a financial boom. The 20th century brought another financial boom, a postwar boom, and a dot-com boom (what beyoncé and these billionaires have in common: massive mortgages). by Jan Kregel in Levy Economics Institute Working Paper, April 2008 The paper supplies a background to the forces that have actually produced today system of property housing financing, the reasons for the current crisis in mortgage financing, and the effect of the crisis on the total monetary system (who has the lowest apr for mortgages). by Atif R. What Does What Are The Types Of Reverse Mortgages Do?

The recent sharp increase in mortgage defaults is significantly amplified in subprime zip codes, or zip codes with a disproportionately large share of subprime customers as . how much is mortgage tax in nyc for mortgages over 500000:oo... by Yuliya Demyanyk in Federal Reserve Bank of St. Louis st thomas timeshare Regional Financial Expert, October 2008 One might http://cristianglum228.wpsuo.com/an-unbiased-view-of-how-to-add-dishcarge-of-mortgages-on-a-resume anticipate to discover a connection between debtors' FICO ratings and the incidence of default and foreclosure during the current crisis. by Geetesh Bhardwaj and Rajdeep Sengupta in Federal Reserve Bank of St - how to reverse mortgages work if your house burns. Louis Working Paper, October 2008 This paper shows that the factor for prevalent default of home loans in the subprime market was an unexpected turnaround in the house price appreciation of the early 2000's. Using loan-level information on subprime mortgages, we observe that the majority of subprime loans were hybrid adjustable rate home mortgages, designed to impose significant monetary ... Kocherlakota in Federal Reserve Bank of Minneapolis, April 2010 Speech prior to the Minnesota Chamber of Commerce by Souphala Chomsisengphet and Anthony Pennington-Cross in Federal Reserve Bank of St. Louis Review, January 2006 This paper describes subprime loaning in the home loan market and how it has actually developed through time. Subprime financing has actually introduced a significant quantity of risk-based prices into the home loan market by creating a myriad of costs and product options mainly identified by borrower credit history (home loan and rental payments, foreclosures and bankru ... An additional charge could also be imposed in case of a redraw. Under the National Credit Code, penalties for early repayment are illegal on brand-new loans given that September 2012; however, a bank might charge a reasonable administration fee for preparation of the discharge of home loan. All reverse home mortgages written since September 2012 should have a "No Negative Equity Warranty". Retrieved 31 January 2017. " Text of S. 825 (100th): Real Estate and Neighborhood Advancement Act of 1987 (Passed Congress/Enrolled Expense version) - GovTrack. us". GovTrack. us. Obtained 2015-12-22. "- REVERSE MORTGAGES: POLISHING NOT TARNISHING THE GOLDEN YEARS". www. gpo.gov. Recovered 2015-12-23. " Reverse Home Mortgage Scams". FBI (Rip-offs and Safety/Common Frauds and Crimes). HUD.gov. 12 U.S.C. 1715z-20( b)( 1 ); 24 C.F.R. 206. 33. (PDF). 12 U.S.C. 1715z-20( b)( 4) 12 U.S.C. 1715z-20( d)( 3 ). " FHA's Home Equity Conversion Home Loan Program". United States Department of Housing and Urban Advancement. 14 October 2010. Archived from the initial on 2012-09-06. Retrieved 11 September 2012. " Reverse Mortgage: What is it and how does it work? 2016-10". 2014-06-11. Retrieved 2014-07-03. (PDF). " MyHECM Principal Limit Calculator". HUD Mortgagee Letter 2014-12 (June 27, 2014) " How Reverse Home Loans Work". AARP.com. March 2010. Retrieved 11 September 2012. (PDF). " Archived copy". Archived from the original on 2010-06-14. Recovered 2009-06-06. CS1 maint: archived copy as title (link) Ecker, Elizabeth (2013-11-06). " Texas Votes "Yes" to Allow Reverse Mortgage For Purchase Item". All About What Happens myrtle beach timeshare rentals To Mortgages In Economic Collapse

Sheedy, Rachel L. (January 2013). " Purchase a Home With a Reverse Mortgage". Kiplinger's Retirement Report. Retrieved 2014-01-10. Coates, Tara (11 February 2011). " 10 Things You Need To Know About Reverse Mortgages: Prior to you sign, ensure you learn about limitations, charges". AARP.com. Reverse Home Mortgages: A Lawyer's Guide. American Bar Association. 1997.

AARP. 12 U.S.C. 1715z-20( j). (PDF). See Home Equity Conversion Mortgages Month-to-month Report (May 2010), http://www. hud.gov/ offices/hsg/comp/ rpts/hecm/hecmmenu. cfm Archived 2010-05-28 at the Wayback Device Pub. L. No. 109-289, s. 131 (2006 ). See for instance the Omnibus Appropriations Act, 2009, Pub. L. No. 111-8, s. 217 (Mar. 11, 2009). For HUD's HECM Summary Reports, see http://www. cfm Archived 2015-09-24 at the Wayback Maker, United States Census Bureau, 2000-01-13. Accessed 2015-06-30. Archived 2015-09-24 at the Wayback Maker Forecasts of the Total Local Population by 5-Year Age Groups, and Sex with Special Age Categories: Middle Series, 2025 to 2045], United States Census Bureau, 2000-01-13. Accessed 2015-06-30. " National Retirement Danger Index Center for Retirement Research".

Some Known Facts About Which Of The Following Is Not A Guarantor Of Federally Insured Mortgages?.

bc.edu. Recovered 2016-07-14. " Working Paper: HECM Reverse Mortgages: Is Market Failure Fixable? - Zell/Lurie Center". realestate. wharton.upenn. edu. Retrieved 2016-07-14. HKMC Reverse Home Mortgage Programme - http://www. hkmc.com. hk/eng/our _ business/reverse _ mortgage_programme. html " Just how much will a reverse mortgage expense?". Customer Financial Security Bureau. Recovered 2020-01-02. Santow, Simon (25 May 2011). " Reverse mortgages grow, but so do warnings". Obtained 12 September 2012. (PDF). June 2012. Retrieved 12 September 2012. Hallman, Ben (27 June 2012). " Reverse Home Mortgage Foreclosures Rising, Seniors Targeted For Scams". Huffington Post. Obtained 12 September 2012. " Reverse Home loans Are Not the Next Sub-Prime". mtgprofessor. com. Editorial Note: Credit Karma receives payment from third-party marketers, however that does not affect our editors' viewpoints. Our marketing partners don't examine, authorize or endorse our editorial material. It's accurate to the very best of our understanding when posted. Availability of items, features and discounts may differ by state or territory. Read our Editorial Guidelines to discover more about our group. What Is The Interest Rate On Mortgages Today - Questions

It's pretty simple, in fact. The offers for monetary products you see on our platform originated from business who pay us. The money we make helps us provide you access to complimentary credit history and reports and assists us develop our other fantastic tools and instructional materials - what kind of mortgages are there. Compensation may factor into how and where items appear on our platform (and in what order). That's why we offer functions like your Approval Chances and cost savings estimates. Of course, the deals on our platform do not represent all financial products out there, however our objective is to reveal you as lots of fantastic options as we can. Whether it's the familiar environment, the surrounding community or the emotional value of the home itself, numerous factors add to elders wanting to stay in their homes for as long as possible. Reverse mortgages are loans that allow seniors to use the house equity they've developed without needing to sell their home. And unlike traditional loans, where you make month-to-month payments versus the principal and interest, with a reverse mortgage you just pay back the principal and interest as soon as you sell or move completely from the house. Our How Did Subprime Mortgages Contributed Additional reading To The Financial Crisis Ideas

If this holds true, you probably own a large percentage if not all of your home. The present market price of your house minus what you still owe on the home (if anything) is called your equity. To discover how much equity you have in your home, deduct the staying balance of your mortgage (the amount you still owe to the loan provider) from your house's existing value. Here are two common ways you can borrow against this equity: home equity loans and reverse mortgages. In order for you to get a home equity loan, lenders typically need you have a stable source of earnings so that you'll have the ability to make month-to-month payments. Considering that numerous elders are retired and on a restricted spending plan, they may not certify. To qualify for a house equity conversion home loan, the most common kind of reverse home mortgage, you should be at least 62 years of ages and either own your home outright or have a home loan with a low balance, along with fulfilling a number of other requirements, like the home being your principal residence and staying so. Indicators on What Are Current Interest Rates On Mortgages You Need To Know

There are a couple of methods you can take the loan, including as one swelling amount in advance, as a credit line that you make use of as needed until you've used up the line of credit, or as routine month-to-month payments. Reverse mortgages typically have variable rates of interest, but home equity conversion mortgages can use set rates. Instead, you are accountable for paying back the loan once you move permanently or offer the house. Or your estate can settle the loan once you die. This all sounds respectable, right? Just remember that while you're not responsible for paying principal or interest on a regular monthly basis, you are accountable for keeping current with your property taxes, homeowners insurance coverage and residential or commercial property maintenance. Now that we have actually got the essentials down, let's go into the information. how do down payments work on mortgages. There are three sort of reverse mortgages: single-purpose, proprietary and home equity conversion home mortgage. If you need money for a particular purpose, like a house improvement, a single-purpose reverse home loan might be an excellent option for you. These loans are provided by some nonprofits and state and local government firms to enable customers to do things such as https://marcodzhq045.mozello.com/blog/params/post/2915533/facts-about-what-is-the-interest-rate-today-on-mortgages-uncovered keep their residential or commercial properties, make clinically essential house improvements like wheelchair ramps, or pay their real estate tax. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed